UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 30, 2018

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 001-14543

____________________________________

TrueBlue, Inc.

(Exact name of registrant as specified in its charter)

______________________________________

|

| | |

Washington | | 91-1287341 |

(State of incorporation) | | (I.R.S. Employer Identification No.) |

| |

1015 A Street, Tacoma, Washington | | 98402 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (253) 383-9101

______________________________________

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

Title of each class | | Name of each exchange on which registered |

Common Stock no par value | | The New York Stock Exchange |

Securities registered under Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| | | | | | |

Large accelerated filer | x | Accelerated filer | ¨ | Non-accelerated filer | ¨ | |

Smaller reporting company | ¨ | Emerging growth company | ¨ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

As of July 1, 2018, the aggregate market value (based on the NYSE quoted closing price) of the common stock held by non-affiliates of the registrant was approximately $1.1 billion.

As of January 31, 2019, there were 40,074,000 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this report is incorporated by reference from the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders scheduled to be held May 15, 2019, which will be filed no later than 120 days after the end of the fiscal year to which this report relates.

TrueBlue, Inc.

Table of Contents

|

| | |

| | Page |

PART I |

Item 1. | | |

Item 1A. | | |

Item 1B. | | |

Item 2. | | |

Item 3. | | |

Item 4. | | |

PART II |

Item 5. | | |

Item 6. | | |

Item 7. | | |

Item 7A. | | |

Item 8. | | |

Item 9. | | |

Item 9A. | | |

| | |

| | |

Item 9B. | | |

PART III |

Item 10. | | |

Item 11. | | |

Item 12. | | |

Item 13. | | |

Item 14. | | |

PART IV |

Item 15. | | |

| | |

| | |

PART I

COMMENT ON FORWARD LOOKING STATEMENTS

Certain statements in this Form 10-K, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements involve risks and uncertainties, and future events and circumstances could differ significantly from those anticipated in the forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “goal,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from those expressed or implied in our forward-looking statements, including the risks and uncertainties described in “Risk Factors” (Part I, Item 1A of this Form 10-K), “Quantitative and Qualitative Disclosures about Market Risk” (Part II, Item 7A of this Form 10-K), and “Management’s Discussion and Analysis” (Part II, Item 7 of this Form 10-K). We undertake no duty to update or revise publicly any of the forward-looking statements after the date of this report, to conform such statements to actual results or to changes in our expectations, whether because of new information, future events, or otherwise.

OUR COMPANY

TrueBlue, Inc. (the “company,” “TrueBlue,” “we,” “us” and “our”) is a leading provider of specialized workforce solutions that help clients achieve growth and improve productivity. We connected approximately 730,000 people with work during fiscal 2018, and served approximately 151,000 clients in a wide variety of industries through our PeopleReady segment which offers industrial staffing services, our PeopleManagement segment which offers contingent and productivity-based on-site industrial staffing services, and our PeopleScout segment which offers recruitment process outsourcing (“RPO”) and managed service provider (“MSP”) services. We are headquartered in Tacoma, Washington.

We began operations in 1989, specializing in on-demand general labor staffing services with the objective of providing clients with talent and flexible workforce solutions to enhance the performance of their businesses. We expanded our on-demand, general labor staffing services through organic geographic expansion throughout the United States, Canada and Puerto Rico. Commencing in 2004, we began expanding through acquisitions to provide a full range of blue-collar staffing solutions, and to help our clients be more productive with a reliable contingent labor workforce and rapidly respond to changing business needs. Commencing in 2014, we expanded through acquisitions to provide complementary outsourced service offerings in permanent employment RPO and employer recruitment branding services, as well as outsourced management of client’s contingent labor vendors.

BUSINESS OVERVIEW

We report our business as three distinct reportable segments described below and in Note 17: Segment Information, to our consolidated financial statements found in Part II, Item 8 of this Annual Report on Form 10-K.

PeopleReady provides access to reliable workers in the United States, Canada and Puerto Rico through a wide range of staffing solutions for on-demand contingent general and skilled labor. PeopleReady connects people to work in a broad range of industries that include construction, manufacturing and logistics, warehousing and distribution, waste and recycling, energy, retail, hospitality, and others.

PeopleReady helped approximately 150,000 clients in fiscal 2018 to be more productive by providing easy access to dependable, blue-collar contingent labor. Through our PeopleReady service line, we connected approximately 310,000 people with work in fiscal 2018. We have a network of 620 branches across all 50 states, Canada and Puerto Rico. Complementing our branch network is our mobile application, JobStackTM, which algorithmically connects workers with jobs, creates a virtual exchange between our workers and clients, and allows our branch resources to expand their recruiting and sales efforts and service delivery. JobStack is increasing the competitive differentiation of our services, expanding our reach into new demographics, and improving both service delivery and work order fill rates.

PeopleManagement provides contingent and productivity-based on-site industrial workforce solutions. In comparison with PeopleReady, services are larger in scale, longer in duration, and provided at the client’s facility.

We use the following distinct brands to market our PeopleManagement contingent workforce solutions:

| |

• | Staff Management | SMX specializes in exclusive outsourced recruitment and on-premise management of the entire facility’s contingent industrial workforce, full shifts or complete functions of the industrial operations. We work closely with on-site management as an integral part of the production and logistics process. We provide scalable solutions to meet the volume requirements in labor-intensive manufacturing, warehousing and logistics. On-premise staffing is large-scale sourcing, screening, recruiting and management of the contingent workforce at a client’s facility in order to achieve faster hiring, lower total cost of workforce, increased safety and compliance, improved retention, greater volume flexibility, and enhanced strategic decision-making through robust reporting and analytics. Client contracts are generally multi-year in duration and pricing is typically based on an hourly rate per contingent worker. Pricing is impacted by factors such as geography, volume, job type, and degree of recruiting difficulty; |

| |

• | SIMOS Insourcing Solutions (“SIMOS”) specializes in exclusive outsourced recruitment and on-premise management of the entire warehouse operations or parts of warehouse operations in order to reduce costs and improve performance. SIMOS systematically analyzes and improves business processes in a client’s facilities and manages the contingent workforce with incentives to drive performance improvements in cost, quality and on-time delivery. Our unique productivity model incorporates fixed price-per-unit solutions to drive client value. Additionally, our continuous analysis and improvement of processes and incentive pay drives workforce efficiency, reduces costs, lowers risk of injury and damage, and improves productivity and service levels; |

| |

• | Centerline Drivers (“Centerline”) specializes in providing dedicated and temporary truck drivers to the transportation and distribution industries. Centerline delivers compliant drivers specifically matched to each client’s needs, allowing them to improve productivity, control costs and deliver improved service. |

Effective March 12, 2018, we divested the PlaneTechs business. For additional information, see Note 3: Acquisitions and Divestiture, to our consolidated financial statements found in Part II, Item 8 of this Annual Report on Form 10-K.

PeopleScout provides permanent employee RPO for our clients. Our RPO solution serves many major industries and job types. Our RPO solution delivers improved talent quality and candidate experience, faster hiring, increased scalability, reduced turnover, lower cost of recruitment, greater flexibility, and increased compliance. We leverage our proprietary AffinixTM technology platform for sourcing, screening and delivering a permanent workforce, along with dedicated service delivery teams to work as an integrated partner with our clients in providing end-to-end talent acquisition services from employer branding, to candidate sourcing and engagement, through onboarding employees. Our solution is highly scalable and flexible, allowing for outsourcing of all or a subset of skill categories across recruitment marketing and a series of recruitment processes and onboarding steps. Client contracts are generally multi-year in duration and pricing is typically composed of a fee for each hire and talent consulting fees. Pricing is impacted by factors such as geography, volume, job type, degree of recruiting difficulty, and the scope of outsourced recruitment and employer branding services included.

PeopleScout also includes our MSP business which manages our clients’ contingent labor programs including vendor selection, performance management, compliance monitoring and risk management. As the client’s exclusive MSP, we have dedicated service delivery teams which work as an integrated partner with our client to increase the productivity of their contingent workforce program.

Effective June 12, 2018, we acquired TMP Holdings LTD (“TMP”) through our PeopleScout subsidiary. Accordingly, the results associated with the acquisition are included in our PeopleScout operating segment. TMP is a mid-sized RPO and employer branding practice operating in the United Kingdom, which is the second largest RPO market in the world. This acquisition increases our ability to win multi-continent engagements by adding a physical presence in Europe, referenceable clients and employer branding capabilities. For additional information, see Note 3: Acquisitions and Divestiture, to our consolidated financial statements found in Part II, Item 8 of this Annual Report on Form 10-K.

INDUSTRY AND MARKET DYNAMICS

The staffing industry, which includes our PeopleReady and PeopleManagement services, supplies contingent workforce solutions to minimize the cost and effort of hiring and managing permanent employees. This allows for rapid response to changes in business conditions through the ability to replace absent employees, fill new positions, and convert fixed or permanent labor costs to variable costs. Staffing companies act as intermediaries in matching available temporary workers to employer work assignments. The work assignments vary widely in duration, skill level, and required experience. The staffing industry is large and highly fragmented with many competing companies. No single company has a dominant share of the industry. Staffing companies compete both to recruit and retain a supply of temporary workers, and to attract and retain clients who will employ these workers. Client demand for contingent staffing services is dependent on the overall strength of the economy and workforce flexibility trends. This creates volatility for the staffing industry based on overall economic conditions. Historically, in periods of economic growth, the number of companies providing contingent workforce solutions has increased due to low barriers to entry whereas during recessionary periods, the number of companies has decreased through consolidation, bankruptcies, or other events.

Our solutions address the following key trends contributing to anticipated staffing growth:

| |

• | Workforce flexibility: The staffing industry continues to experience increased demand in relation to total job growth as demand for a flexible workforce continues to grow with competitive and economic pressures to reduce costs, meet dynamic seasonal demands, and respond to rapidly changing market conditions. |

| |

• | Workforce productivity: Companies are under increasing competitive pressures to improve productivity through workforce solutions that improve performance. |

| |

• | Worker preferences and access to talent: Workers are demanding more flexibility in how, when and where they work as well as access to contingent work opportunities through mobile technology. Baby boomers are leaving the workforce and leaving a talent shortage in what have traditionally been blue-collar trades. The remaining workers are in greater demand and have more power to find the employment situation they want or stay busy working on a contingent basis. |

The human resource outsourcing industry involves transitioning various functions handled by internal human resources and labor procurement to outside service providers on a permanent or project basis. Human resource departments are faced with increasingly complex operational and regulatory requirements, a tightening labor market, increased candidate expectations, an expanding talent technology landscape, and pressure to achieve efficiencies, which increase the need to migrate non-core functions to outsourced providers. The human resource outsourcing industry includes RPO and MSP solutions which allow clients to more effectively find and engage high-quality talent, leverage talent acquisition technology, and scale their talent acquisition function to keep pace with changing business needs. PeopleScout is a leader in RPO and MSP services, which are in the early stages of their adoption cycles, and therefore, we believe they continue to have significant growth potential.

Our solutions address the following key trends contributing to anticipated RPO growth:

| |

• | Talent access and engagement: As competition for qualified candidates increases, clients are relying on RPO providers to elevate the employer brand, build talent communities, create a world class candidate experience, leverage innovative talent technology, and facilitate effective recruitment marketing and candidate communication strategies. |

| |

• | Leveraging talent acquisition technology: Automation, artificial intelligence and machine learning are transforming talent acquisition, and the fragmented talent technology ecosystem is becoming more crowded, with significant investments flowing in and new technology coming online rapidly. RPO providers are continuously identifying, evaluating and investing in new technology to leverage as part of their talent technology stack to best meet today’s candidate’s expectations of a personalized, mobile-optimized and efficient hiring process. RPO providers are uniquely positioned to successfully integrate and deploy new talent technology based on the volume of candidate engagements they manage and their understanding of the talent landscape, thereby reducing the investments required to be made by clients. |

| |

• | Scalability: RPO providers can add significant scalability to a company’s recruiting and hiring efforts, including accommodating seasonal, project or peak hiring needs without sacrificing quality. Providers also help clients increase efficiency and drive better performance by standardizing processes and reducing time to fill and onboard the best fit talent into a client’s organization, and enabling clients to focus on their core business. |

Our solutions address the following key trends contributing to anticipated MSP growth:

| |

• | Vendor consolidation and cost savings: As an organization’s spend on contingent workforce rises, it becomes increasingly interested in reducing the administrative burden of managing multiple outside vendors, having consistency among contractors and processes, and maintaining robust performance tracking and analytics. Vendor consolidation can achieve significant efficiencies through enhanced scale and cost advantages such as single point of contact, standardized contracts, and consolidated invoicing and reporting. |

| |

• | Access to talent: An MSP solution allows a company access to a large variety of staffing vendors with the efficiency of working with one supplier. An MSP can access numerous vendors to find the best talent at the best price more quickly, thereby delivering a better outcome for the client. |

| |

• | Compliance pressure: Demand for temporary employee sourcing and workforce vendor management solutions is driven by increasing work eligibility legislation and compliance monitoring to ensure correct worker classification in order to properly address tax withholding, overtime, Social Security, unemployment and health care obligations to avoid government penalties and lawsuits. |

BUSINESS STRATEGY

Market leadership through organic growth of our specialized workforce solutions

Our clients have a variety of challenges in running their businesses, many of which are unique to the industries in which they operate, their competitive pressures, and business performance. We are industry leaders dedicated to staffing solutions tailored to our clients’ needs and the industries in which they operate. Our differentiated solutions keep pace with their changing needs and are as follows:

| |

• | We will continue to evaluate opportunities to expand our market presence for specialized blue-collar staffing services and expand our geographical reach through new physical locations, expand use of existing locations to provide the full range of blue-collar staffing services, and dispatch of our temporary workers to areas without branches. Continued investment in specialized sales, recruiting and service expertise will create a more seamless experience for our clients to access all of our services with more comprehensive solutions to enhance their performance and our growth. Our service lines offer complementary workforce solutions with unique value propositions to meet our clients’ demand for talent. |

| |

• | We will continue to invest in technology that increases our ability to attract more clients and employees as well as reduce the cost of delivering our services. We are committed to leveraging technology to improve the temporary worker and client experience. Our technological innovation makes it easier for our clients to do business with us and easier to connect workers to work opportunities. We are making significant investments in online and mobile applications to improve the access, speed and ease of connecting our clients with both high-quality temporary and permanent employee workforce solutions. |

| |

◦ | We introduced our mobile application, JobStack, and completed the roll out to our temporary workers in 2017. We rolled out JobStack to our clients in 2018 and now over 30% of all PeopleReady jobs are filled through JobStack. This has created a virtual exchange between our workers and clients, which allows our branch resources to expand their recruiting and sales efforts and service delivery. JobStack is increasing the competitive differentiation of our services, expanding our reach into new demographics, and improving both service delivery and work order fill rates. We will be adding functionality to further enhance both client and associate retention. |

| |

◦ | We introduced a mobile-first, cloud-based proprietary platform, Affinix, in 2017 for sourcing, screening and delivering a permanent workforce. Affinix creates a consumer-like candidate experience and streamlines the sourcing process. Affinix delivers speed and scalability while leveraging recruitment marketing, machine learning, predictive analytics and other emerging technology to make the end-to-end process seamless for the candidate. |

| |

• | We are well positioned for growth by providing our clients with the talent and flexible workforce solutions they need to enhance business performance. With growing demand for improved productivity and accessing temporary workers, our clients are looking for a full range of workforce services. |

| |

• | We are recognized as an industry leader for RPO services. The RPO industry is in the early stages of its adoption cycle, and therefore, we believe it has significant growth potential. The success of early adopters is generating greater opportunity to expand our service offering. We have a differentiated service that leverages innovative technology for high-volume sourcing and dedicated client service teams for connecting people to opportunities. We have a track record of helping our clients reduce the cost of hiring, add significant scalability to recruiting and hiring, and access numerous sources to prospect for the best talent quickly, thereby delivering a better outcome for the client. Companies are facing rapidly changing employment demographics, a shortage of talent, and dynamic changes to how people connect to work opportunities. Our solution addresses these growing challenges. We expanded our services with the TMP acquisition. TMP is a mid-sized RPO and employer branding practice operating in the United Kingdom, which is the second largest RPO market in the world. This acquisition increases our ability to win multi-continent engagements by adding a physical presence in Europe, referenceable clients, and employer branding capabilities. |

| |

• | Our MSP solution is focused on domestic middle-market companies with a growing dependence on contingent labor. Our managed service provider solutions have enabled our clients to efficiently source, engage, fulfill, measure and manage all categories of contingent and externally sourced labor. We believe our MSP solution is uniquely positioned to manage the full range of our clients’ labor needs. |

Growth through strategic acquisitions

Strategic acquisitions continue to be a key growth strategy with a focus on globalizing our RPO services. We believe we have a core competence in assessing, valuing and integrating acquisitions culminating in higher shareholder returns. We are excited about the future of human resource outsourcing and believe we can continue to create shareholder value through acquisitions, which expand our service offerings in high-growth markets, enhance our use of technology to better serve our clients, and increase our own efficiency.

CLIENTS

Our clients range from small and medium-sized businesses to Fortune 100 companies.

During fiscal 2018, we served approximately 151,000 clients in industries including construction, energy, manufacturing, warehousing and distribution, waste and recycling, energy, transportation, retail, hospitality, general labor, and many more. Our ten largest clients accounted for 16.1% of total revenue for fiscal 2018, 17.6% for fiscal 2017 and 19.9% for fiscal 2016. Our single largest client for fiscal 2018 accounted for 2.9% of total company revenue.

No single client represented more than 10.0% of total company revenue for fiscal 2018, 2017 or 2016.

EMPLOYEES

As of December 30, 2018, we employed approximately 6,700 full-time equivalent employees.

TEMPORARY WORKERS

We recruit temporary workers daily so that we can be responsive to the planned and unplanned needs of the clients we serve. We attract our pool of temporary workers through our proprietary mobile applications, online resources, extensive internal databases, advertising, job fairs and various other methods. We identify the skills, knowledge, abilities and personal characteristics of a temporary worker and match their competencies and capabilities to a client’s requirements. This enables our clients to obtain immediate value by placing a highly productive employee on the job site. We use a variety of proprietary programs and methods for identifying and assessing the skill level of our temporary workers when selecting a particular individual for a specific assignment and retaining those workers for future assignments. We believe that our programs and methods enable us to offer a higher quality of service by increasing productivity, decreasing turnover, reducing absenteeism, and improving worker safety.

We provide a bridge to permanent, full-time employment for thousands of temporary workers each year. Workers also come to us because of the flexibility we offer to fill a short-term financial need and/or provide longer-term contingent flexible labor opportunities. Workers may be assigned to different jobs and job sites, and their assignments could last for as little as a few hours or extend for several weeks or months. We provide our workers meaningful work and the opportunity to improve their skills. We are considered the legal employer of our workers, and laws regulating the employment relationship are applicable to our operations. We consider our relations with our temporary workers to be good.

We remain focused and committed to worker safety. We have developed an integrated risk management program that focuses on loss analysis, education and safety improvement programs to reduce our operational costs and risk exposure. We regularly analyze our workers’ compensation claims to identify trends. This allows us to focus our resources on those areas that may have the greatest impact on us, price our services appropriately, and adjust our sales and operational approach in these areas. We have also developed educational materials for distribution to our clients and workers to address specific safety risks unique to their industry.

COMPETITION

Contingent staffing services

The strongest staffing services competitor in a particular market is a company with established relationships and a track record of meeting the client’s needs. We compete with other large publicly-held staffing companies as well as privately-owned staffing companies on a national, regional and local level. We also experience competition from internet-based companies providing a variety of flexible workforce solutions. Competition exists in attracting clients as well as qualified temporary workers for our clients. No single company has a dominant share of the industry. Competitive forces have historically limited our ability to raise our prices to immediately and fully offset increased costs of doing business, some of which include increased temporary worker wages, costs for workers’ compensation, unemployment insurance and health care.

The most significant competitive factors are price, ability to promptly fill client orders, success in meeting clients’ expectations of recruiting temporary workers, and appropriately addressing client service issues. We believe we derive a competitive advantage from our service history and our specialized approach in serving the industries of our clients. Our national presence, industry specialization, investment in technology, and proprietary systems and processes, together with specialized programs focused on worker safety, risk management, and legal and regulatory compliance are key differentiators from many of our competitors.

Human resource outsourcing

The strongest competitors are companies specializing in RPO services and business process outsourcing companies that also offer RPO services. No one provider dominates the market. Competition also includes internal human resource departments that have not or are not considering outsourcing. The most significant competitive factors for RPO services are the ability to reduce client cost by deploying an RPO solution and reducing the internal human resource cost structure of our clients. Important factors for success in RPO services include the ability to add significant scalability to a client’s recruiting and hiring efforts, including accommodating seasonal and irregular hiring; the ability to increase efficiency by standardizing processes and facilitating transitions for candidates and employees; and the ability to source the most attractive talent at the best price. Our tailored solutions, client partnership, proprietary technology and service delivery are key differentiators from many of our competitors.

CYCLICAL AND SEASONAL NATURE OF OUR BUSINESS

The workforce solutions business has historically been cyclical, often acting as an indicator of both economic downturns and upswings. Clients tend to use temporary workers to supplement their existing workforce and generally hire permanent workers when long-term demand is expected to increase. As a consequence, our revenues tend to increase quickly when the economy begins to grow. Conversely, our revenues also decrease quickly when the economy begins to weaken and thus temporary staff positions are eliminated, permanent hiring is frozen, and turnover replacement diminishes.

Our business experiences seasonal fluctuations for contingent staffing services. Demand is lower during the first and second quarters, in part due to limitations to outside work during the winter months and slowdown in manufacturing and logistics after the holiday season. Our working capital requirements are primarily driven by temporary worker payroll and client accounts receivable. Since receipts from clients lag payroll to temporary workers, working capital requirements increase substantially in periods of growth. Demand for contingent labor peaks during the third quarter for outdoor work and the fourth quarter for manufacturing, assembly, warehousing, distribution and logistics for the holiday season.

REGULATION

Our services are subject to a variety of complex federal and state laws and regulations. We continuously monitor legislation and regulatory changes for their potential effect on our business. We invest in technology and process improvements to implement required changes while minimizing the impact to our operating efficiency and effectiveness. Regulatory cost increases are passed through to our clients to the fullest extent possible.

FINANCIAL INFORMATION ABOUT GEOGRAPHIC AREAS

For information regarding revenue from operations and long-lived assets by domestic and foreign operations, please refer to the information presented in Note 17: Segment Information, to our consolidated financial statements found in Part II, Item 8 of this Annual Report on Form 10-K.

AVAILABLE INFORMATION

Our Annual Report on Form 10-K, along with all other reports and amendments filed with or furnished to the Securities and Exchange Commission (“SEC”), are publicly available, free of charge, on our website at www.trueblue.com as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. Our Corporate Governance Guidelines, Code of Business Conduct and Ethics and Board Committee Charters are also posted to our website. The information on our website is not part of this or any other report we file with, or furnish to, the SEC.

Investing in our securities involves risk. The following risk factors and all other information set forth in this Annual Report on Form 10-K should be considered in evaluating our future prospects. If any of the events described below occur, our business, financial condition, results of operations, liquidity, or access to the capital markets could be materially and adversely affected.

Demand for our workforce solutions is significantly affected by fluctuations in general economic conditions.

The demand for workforce solutions is highly dependent upon the state of the economy and upon the workforce needs of our clients, which creates uncertainty and volatility. National and global economic activity can be slowed by many factors, including rising interest rates and global trade uncertainties. As economic activity slows, companies tend to reduce their use of temporary workers and reduce their recruitment of new employees. Significant declines in demand of any region or industry in which we have a major presence may severely reduce the demand for our services and thereby significantly decrease our revenues and profits. Deterioration in economic conditions or the financial or credit markets could also have an adverse impact on our clients’ ability to pay for services we have already provided.

It is difficult for us to forecast future demand for our services due to the inherent uncertainty in forecasting the direction and strength of economic cycles and the project nature of our staffing assignments. The uncertainty can be exacerbated by volatile economic conditions, which may cause clients to reduce or defer projects for which they utilize our services. The negative impact to our business can occur before a decline in economic activity is seen in the broader economy. When it is difficult for us to accurately forecast future demand, we may not be able to determine the optimal level of personnel and investment necessary to profitably take advantage of growth opportunities.

We may be unable to attract sufficient qualified candidates to meet the needs of our clients.

We compete to meet our clients’ needs for workforce solutions and, therefore, we must continually attract qualified candidates to fill positions. Attracting qualified candidates depends on factors such as desirability of the assignment, location, and the associated wages and other benefits. We have experienced shortages of qualified candidates and we may experience such shortages in the future. Further, if there is a shortage, the cost to employ or recruit these individuals could increase. If we are unable to pass those costs through to our clients, it could materially and adversely affect our business. Organized labor periodically engages in efforts to represent various groups of our temporary workers. If we are subject to unreasonable collective bargaining agreements or work disruptions, our business could be adversely affected.

We may not achieve the intended effects of our business strategy which could negatively impact our results.

Our business strategy focuses on driving growth in our PeopleReady, PeopleManagement and PeopleScout business lines by investing in innovative technology, acquisitions, and initiatives which drive organic growth. Our investments and acquisitions may not achieve our desired returns and the results of our initiatives may not be as expected or may be impacted by matters outside of our control. If we are unsuccessful in executing any of these strategies, we may not achieve our goal of revenue and profitability growth, which could negatively impact financial results.

Our workforce solutions are subject to extensive government regulation and the imposition of additional regulations, which could materially harm our future earnings.

Our workforce solutions are subject to extensive government regulation. The cost to comply, and any inability to comply with government regulation, could have a material adverse effect on our business and financial results. Increases or changes in government regulation of the workplace or of the employer-employee relationship, or judicial or administrative proceedings related to such regulation, could materially harm our business.

Our temporary staffing services employ temporary workers. The wage rates we pay to temporary workers are based on many factors including government-mandated minimum wage requirements, payroll-related taxes and benefits. If we are not able to increase the fees charged to clients to absorb any increased costs related to these factors, our results of operations and financial condition could be adversely affected.

We offer our temporary workers in the United States government-mandated health insurance in compliance with the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 (collectively, the “ACA”). Because the requirements, regulations, and interpretations of the ACA may change, the ultimate financial effect of the ACA is not yet known, and changes in its requirements and interpretations could increase or change our costs. In addition, because of the uncertainty surrounding a potential repeal or replacement of the ACA, we cannot predict with any certainty the likely impact of the ACA’s repeal or the adoption of any other health care reform legislation on our financial condition or operating results. Whether or not there is a change in health care legislation in the United States, there is likely to be significant disruption to the health care market in the future, and the costs of our health care expenditures may increase. If we are unable to comply with changes to the ACA, or any future health care legislation in the United States, or sufficiently raise the rates we charge our clients to cover any additional costs, such noncompliance or increases in costs could materially harm our business.

We may incur employment related claims and costs that could materially harm our business.

We are in the business of employing people in the workplaces of our clients. We incur a risk of liability for claims for personal injury, wage and hour violations, immigration, discrimination, harassment, and other liabilities arising from the actions of our clients and/or temporary workers. Some or all of these claims may give rise to negative publicity, litigation, settlements, or investigations. We may incur costs, charges or other material adverse impacts on our financial statements for the period in which the effect of an unfavorable final outcome becomes probable and can be reasonably estimated.

We maintain insurance with respect to some potential claims and costs with deductibles. We cannot be certain that our insurance will be available, or if available, will be in sufficient amount or scope to cover all claims that may be asserted against us. Should the ultimate judgments or settlements exceed our insurance coverage, they could have a material effect on our business. We cannot be certain we will be able to obtain appropriate types or levels of insurance in the future, that adequate replacement policies will be available on acceptable terms, or at all, or that our insurance providers will be able to pay claims we make under such policies.

We are dependent on workers’ compensation insurance coverage at commercially reasonable terms. Unexpected changes in claim trends on our workers’ compensation may negatively impact our financial condition.

Our temporary staffing services employ workers for which we provide workers’ compensation insurance. Our workers’ compensation insurance policies are renewed annually. The majority of our insurance policies are with AIG. Our insurance carriers require us to collateralize a significant portion of our workers’ compensation obligation. The majority of collateral is held in trust by a third-party for the payment of these claims. The loss or decline in value of the collateral could require us to seek additional sources of capital to pay our workers’ compensation claims. We cannot be certain we will be able to obtain appropriate types or levels of insurance in the future or that adequate replacement policies will be available on acceptable terms. As our business grows or if our financial results deteriorate, the amount of collateral required will likely increase and the timing of providing collateral could be accelerated. Resources to meet these requirements may not be available. The loss of our workers’ compensation insurance coverage would prevent us from operating as a staffing services business in the majority of our markets. Further, we cannot be certain that our current and former insurance carriers will be able to pay claims we make under such policies.

We self-insure, or otherwise bear financial responsibility for, a significant portion of expected losses under our workers’ compensation program. Unexpected changes in claim trends, including the severity and frequency of claims, changes in state laws regarding benefit levels and allowable claims, actuarial estimates, or medical cost inflation, could result in costs that are significantly different than initially reported. There can be no assurance that we will be able to increase the fees charged to our clients in a timely manner and in a sufficient amount to cover increased costs as a result of any changes in claims-related liabilities.

We actively manage the safety of our temporary workers with our safety programs and actively control costs with our network of workers’ compensation related service providers. These activities have had a positive impact creating favorable adjustments to workers’ compensation liabilities recorded in prior periods. The benefit of these adjustments are likely to decline and there can be no assurance that we will be able to continue to reduce accident rates and control costs to produce these results in the future.

We operate in a highly competitive industry and may be unable to retain clients or market share.

Our industry is highly competitive and rapidly innovating, with low barriers to entry. We compete in global, national, regional and local markets with full-service and specialized temporary staffing companies as well as business process outsourcing companies that also offer our services. Our competitors offer a variety of flexible workforce solutions. Therefore, there is no assurance that we will be able to retain clients or market share in the future, nor can there be any assurance that we will, in light of competitive pressures, be able to remain profitable or maintain our current profit margins.

Advances in technology may disrupt the labor and recruiting markets.

We expect the increased use of internet-based and mobile technology will attract additional technology-oriented companies and resources to the staffing industry. Our candidates and clients increasingly demand technological innovation to improve the access to and delivery of our services. Our clients increasingly rely on automation, artificial intelligence and other new technologies to reduce their dependence on labor needs, which may reduce demand for our services and impact our operations. We face extensive pressure for lower prices and new service offerings and must continue to invest in and implement new technology and industry developments in order to remain relevant to our clients and candidates. If we are unable to do so, our business and results of operations may decline materially.

We are at risk of damage to our brands and reputation, which is important to our success.

Our ability to attract and retain clients, temporary workers, candidates, and employees is affected by external perceptions of our brands and reputation. Negative perceptions or publicity could damage our reputation with current or perspective clients and employees. Negative perceptions or publicity regarding our vendors, clients, or business partners may adversely affect our brand and reputation. We may not be successful in detecting, preventing, or negating all changes in or impacts upon our reputation.

Our level of debt and restrictions in our credit agreement could negatively affect our operations and limit our liquidity and our ability to react to changes in the economy.

Extensions of credit under our credit agreement (“Revolving Credit Facility”) are limited. Our Revolving Credit Facility contains restrictive covenants that require us to maintain certain financial conditions. Our failure to comply with these restrictive covenants could result in an event of default, which, if not cured or waived, could result in our being required to repay these borrowings before their due date. We may not have sufficient funds on hand to repay these loans, and if we are forced to refinance these borrowings on less favorable terms, or are unable to refinance at all, our results of operations and financial condition could be materially adversely affected by increased costs and rates.

Our principal sources of liquidity are funds generated from operating activities, available cash and cash equivalents, and borrowings under our Revolving Credit Facility. We must have sufficient sources of liquidity to meet our working capital requirements, fund our workers’ compensation collateral requirements, service our outstanding indebtedness, and finance investment opportunities. Without sufficient liquidity, we could be forced to curtail our operations or we may not be able to pursue promising business opportunities.

Our debt levels could have significant consequences for the operation of our business including: requiring us to dedicate a significant portion of our cash flow from operations to servicing our debt rather than using it for our operations; limiting our ability to obtain additional debt financing for future working capital, capital expenditures, or other corporate purposes; limiting our ability to take advantage of significant business opportunities, such as acquisition opportunities; limiting our ability to react to changes in market or industry conditions; and putting us at a disadvantage compared to competitors with less debt.

The loss of, or substantial decline in revenue from, larger clients could have a material adverse effect on our revenues, profitability and liquidity.

We experience revenue concentration with large clients. Generally our contracts do not contain guarantees of minimum duration, revenue levels, or profitability and our clients may terminate their contracts or materially reduce their requested levels of service at any time. The loss of, or reduced demand for our services from, larger clients has had, and in the future could have, a material adverse effect on our business, financial condition and results of operations. In addition, client concentration exposes us to concentrated credit risk, as a significant portion of our accounts receivable may be from a small number of clients. If we are unable to collect our receivables or are required to take additional reserves, our results and cash flows will be adversely affected.

Failure of our information technology systems could adversely affect our operating results.

The efficient operation of our business is dependent on our information technology systems. We rely on our information technology systems to monitor and control our operations, adjust to changing market conditions, implement strategic initiatives, and provide services to clients. We rely heavily on proprietary and third-party information technology systems, mobile device technology and related services, and other technology, which may not yield the intended results. Our systems may experience problems with functionality and associated delays. The failure of our systems to perform as anticipated could disrupt our business and could result in decreased revenue and increased overhead costs, causing our business and results of operations to suffer materially.

Our information technology systems may need to be updated or replaced.

We occasionally implement, modify, retire and change our systems. For example, we are in the process of implementing new cloud-based enterprise resource planning and human capital management systems in 2019. These changes to our information technology systems may be disruptive, take longer than desired, be more expensive than anticipated, be distracting to management, or fail, causing our business and results of operations to suffer materially.

The improper disclosure of, or access to, our confidential and/or proprietary information, or a failure to adequately protect this information, could materially harm our business.

Our business requires the use, processing, and storage of confidential information about applicants, candidates, temporary workers, other employees and clients. We experience cyberattacks, computer viruses, social engineering schemes and other means of unauthorized access to our systems. The security controls over sensitive or confidential information and other practices we and our third-party vendors follow may not prevent the improper access to, disclosure of, or loss of such information. We may fail to implement practices and procedures that comply with increasing international and domestic privacy regulations, such as the General Data Protection Regulations or the California Consumer Privacy Act. Failure to protect the integrity and security of such confidential and/or proprietary information could expose us to regulatory fines, litigation, contractual liability, damage to our reputation and increased compliance costs.

A data breach, or improper disclosure of, or access to our clients’ information could materially harm our business.

Our temporary workers and employees may have access to or exposure to confidential information about applicants, candidates, temporary workers, other employees and clients. The security controls over sensitive or confidential information and other practices we, clients and our third-party vendors follow may not prevent the improper access to, disclosure of, or loss of such information. Failure to protect the integrity and security of such confidential and/or proprietary information could expose us to regulatory fines, litigation, contractual liability, damage to our reputation and increased compliance costs.

Our facilities, operations and information technology systems are vulnerable to damage and interruption.

Our primary computer systems, headquarters, support facilities and operations are vulnerable to damage or interruption from power outages, computer and telecommunications failures, computer viruses, employee errors, security breaches, natural disasters and catastrophic events. Failure of our systems or damage to our facilities may cause significant interruption to our business, and require significant additional capital and management resources to resolve, causing material harm to our business.

Acquisitions and new business initiatives may have an adverse effect on our business.

We expect to continue making acquisitions, adjusting the composition of our business lines, and entering into new business initiatives as part of our business strategy. This strategy may be impeded, however, and we may not achieve our long-term growth goals if we cannot identify suitable acquisition candidates or new business initiatives, or if acquisition candidates are not available under acceptable terms.

Future acquisitions could result in incurring additional debt and contingent liabilities, an increase in interest expense, amortization expense, and charges related to integration costs. Additional indebtedness could also include covenants or other restrictions that would impede our ability to manage our operations. We may also issue equity securities to pay for an acquisition, which could result in dilution to our shareholders. Any acquisitions we announce could be viewed negatively by investors, which may adversely affect the price of our common stock.

New business initiatives and changes in the composition of our business mix can be distracting to our management and disruptive to our operations, causing our business and results of operations to suffer materially. We may have difficulty managing growth or integrating acquired companies into our operating, financial planning, and financial reporting systems. Acquisitions and new business initiatives, including initiatives outside of our workforce solutions business, in new markets, or new geographies, could involve significant unanticipated challenges and risks including not advancing our business strategy, not realizing our anticipated return on investment, experiencing difficulty in implementing initiatives or integrating acquired operations, or directing management’s attention from our other businesses. The potential loss of key executives, employees, clients, suppliers, vendors, and other business partners of businesses we acquire may adversely impact the value of the assets, operations, or business we acquire. These events could cause material harm to our business, operating results, or financial condition.

Our results of operations could materially deteriorate if we fail to attract, develop and retain qualified employees.

Our performance is dependent on attracting and retaining qualified employees who are able to meet the needs of our clients. We believe our competitive advantage is providing unique solutions for each client, which requires us to have trained and engaged employees. Our success depends upon our ability to attract, develop and retain a sufficient number of qualified employees, including management, sales, recruiting, service and administrative personnel. The turnover rate in the employment services industry is high, and qualified individuals of the requisite caliber and number needed to fill these positions may be in short supply. Our inability to recruit, train and motivate a sufficient number of qualified individuals may delay or affect the speed and quality of our strategy execution and planned growth. Delayed expansion, significant increases in employee turnover rates, or significant increases in labor costs could have a material adverse effect on our business, financial condition and results of operations.

We may have additional tax liabilities that exceed our estimates.

We are subject to federal taxes, a multitude of state and local taxes in the United States, and taxes in foreign jurisdictions. We face continued uncertainty surrounding the 2017 Tax Cuts and Jobs Act and any reduction or change in tax credits which we utilize, such as the Work Opportunity Tax Credit. In the ordinary course of our business, there are transactions and calculations where the ultimate tax determination is uncertain. We are regularly subject to audit by tax authorities. Although we believe our tax estimates are reasonable, the final determination of tax audits and any related litigation could be materially different from our historical tax provisions and accruals. The results of an audit or litigation could materially harm our business. The taxing authorities of the jurisdictions in which we operate may challenge our methodologies for valuing intercompany arrangements or may change their laws, which could increase our worldwide effective tax rate and harm our financial position and results of operations.

We cannot guarantee that we will repurchase our common stock pursuant to our share repurchase program or that our share repurchase program will enhance long-term shareholder value.

In September 2017, our Board of Directors authorized a share repurchase program. Under the program, we are authorized to repurchase shares of common stock for an aggregate purchase price not to exceed $100 million, excluding fees, commissions and other ancillary expenses. Although the Board of Directors has authorized a share repurchase program, the share repurchase program does not obligate the company to repurchase any specific dollar amount or to acquire any specific number of shares. The timing and amount of the repurchases, if any, will depend upon several factors, including market and business conditions, the trading price of the company’s common stock and the nature of other investment opportunities. The repurchase program may be limited, suspended or discontinued at any time without prior notice. In addition, repurchases of our common stock pursuant to our share repurchase program could affect our stock price and increase its volatility. The existence of a share repurchase program could cause our stock price to be higher than it would be in the absence of such a program and could potentially reduce the market liquidity for our stock. Additionally, our share repurchase program could diminish our cash reserves, which may impact our ability to finance future growth and to pursue possible future strategic opportunities and acquisitions. There can be no assurance that these share repurchases will enhance shareholder value because the market price of our common stock may decline below the level at which we repurchased shares of stock. Although our share repurchase program is intended to enhance long-term shareholder value, there is no assurance that it will do so and short-term stock price fluctuations could reduce the program’s effectiveness.

Failure to maintain adequate financial and management processes and controls could lead to errors in our financial reporting.

If our management is unable to certify the effectiveness of our internal controls, including those over our third-party vendors, or if our independent registered public accounting firm cannot render an opinion on the effectiveness of our internal controls over financial reporting, or if material weaknesses in our internal controls are identified, we could be subject to regulatory scrutiny and a loss of public confidence. In addition, if we do not maintain adequate financial and management personnel, processes and controls, we may not be able to accurately report our financial performance on a timely basis, which could cause our stock price to fall.

Outsourcing certain aspects of our business could result in disruption and increased costs.

We have outsourced certain aspects of our business to third-party vendors that subject us to risks including disruptions in our business and increased costs. For example, we have engaged third parties to host and manage certain aspects of our data center, information and technology infrastructure, mobile applications, and electronic pay solutions, to provide certain back office support activities, and to support business process outsourcing for our clients. Accordingly, we are subject to the risks associated with the vendors’ ability to provide these services in a manner that meets our needs. If the cost of these services is more than expected, if we or the vendors are unable to adequately protect our data and information is lost, or if our ability to deliver our services is interrupted, then our business and results of operations may be negatively impacted.

If our acquired intangible assets become impaired we may be required to record a significant charge to earnings.

We regularly review acquired intangible assets for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. We test goodwill and indefinite-lived intangible assets for impairment at least annually. Factors that may be considered a change in circumstances, indicating that the carrying value of the intangible assets may not be recoverable, include: macroeconomic conditions, such as deterioration in general economic conditions; industry and market considerations, such as deterioration in the environment in which we operate; cost factors, such as increases in labor or other costs that have a negative effect on earnings and cash flows; our financial performance, such as negative or declining cash flows or a decline in actual or planned revenue or earnings compared with actual and projected results of relevant prior periods; other relevant entity-specific events, such as changes in management, key personnel, strategy, or clients; and sustained decreases in share price. We may be required to record a significant charge in our financial statements during the period in which we determine an impairment of our acquired intangible assets has occurred, therefore negatively impacting our financial results.

Our stock price may be volatile.

Our stock price may experience substantial fluctuation based on a variety of factors, several of which are beyond our control. Some of these factors include general economic conditions; actual or anticipated variations in our quarterly operating results; changes in financial estimates by securities analysts; changes or volatility in the financial markets; announcements by our competitors related to new services or acquisitions; and shareholder activism. Fluctuations in our stock price could mean that investors will not be able to sell their shares at or above the price they paid and may impair our ability in the future to offer common stock as a source of additional capital.

We face risks in operating internationally.

A portion of our business operations and support functions are located outside of the United States. These international operations are subject to a number of risks, including political and economic conditions in those foreign countries, the burden of complying with various foreign laws and technical standards, unpredictable changes in foreign regulations, U.S. legal requirements governing U.S. companies operating in foreign countries, legal and cultural differences in the conduct of business, potential adverse tax consequences and difficulty in staffing and managing international operations. We recently acquired operations in the United Kingdom, which could be negatively impacted as clients in the United Kingdom encounter uncertainties related to the potential exit from the European Union. We could also be exposed to fines and penalties under U.S. or foreign laws prohibiting improper payments to governmental officials and others for the purpose of obtaining or retaining business. Although we have implemented policies and procedures designed to ensure compliance with these laws, we cannot be sure that our employees, contractors or agents will not violate such policies. Any such violations could materially damage our reputation, brands, business and operating results. Further, changes in U.S. laws and policies governing foreign investment and use of foreign operations or workers, and any negative sentiments towards the United States as a result of such changes, could adversely affect our operations.

Foreign currency fluctuations may have a material adverse effect on our operating results.

We report our results of operations in U.S. dollars. The majority of our revenues are generated in the United States. Our international operations are denominated in currencies other than the U.S. dollar, and unfavorable fluctuations in foreign currency exchange rates could have an adverse effect on our reported financial results. Increases or decreases in the value of the U.S. dollar against other major currencies could affect our revenues, operating profit and the value of balance sheet items denominated in foreign currencies. Our exposure to foreign currencies could have an adverse effect on our business, financial condition, cash flow and/or results of operations. Furthermore, the volatility of currencies may impact year-over-year comparability.

|

| |

Item 1B. | UNRESOLVED STAFF COMMENTS |

Not applicable.

We lease the building space at all our PeopleReady branches and other offices except for one that we own in Florida. In addition to branches for our PeopleReady operations, we lease office spaces for our PeopleManagement, PeopleScout and PeopleReady centralized support functions. Under the majority of our PeopleReady branch leases, we have the right to terminate the lease with 90 days notice. We do not anticipate any difficulty in renewing these leases or in finding alternative sites in the ordinary course of business. We own an office building in Tacoma, Washington, which serves as our corporate headquarters. Management believes all our facilities are currently suitable for their intended use.

See Note 10: Commitments and Contingencies, to our consolidated financial statements found in Part II of Item 8 of this Annual Report on Form 10-K.

|

| |

Item 4. | MINE SAFETY DISCLOSURES |

Not applicable.

PART II

|

| |

Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market information

Our common stock is listed on the New York Stock Exchange under the ticker symbol TBI.

Holders of the corporation’s common stock

We had approximately 502 shareholders of record as of January 31, 2019. This number does not include shareholders for whom shares were held in “nominee” or “street name.”

Dividends

No cash dividends have been declared on our common stock to date nor have any decisions been made to pay a dividend in the future. Payment of dividends is evaluated on a periodic basis and if a dividend were paid, it would be subject to the covenants of our revolving credit agreement, which may have the effect of restricting our ability to pay dividends.

Stock repurchases

The table below includes repurchases of our common stock pursuant to publicly announced plans or programs and those not made pursuant to publicly announced plans or programs during the thirteen weeks ended December 30, 2018.

|

| | | | | | | | |

Period | Total number of shares purchased (1) | Weighted average price paid per share (2) | Total number of shares purchased as part of publicly announced plans or programs (3) | Maximum number of shares (or approximate dollar value) that may yet be purchased under plans or programs at period end (4) |

10/01/2018 through 10/28/2018 | 3,017 |

|

| $25.39 |

| — |

| $67.8 million |

10/29/2018 through 11/25/2018 | 1,083 |

|

| $24.14 |

| 205,100 |

| $62.8 million |

11/26/2018 through 12/30/2018 | 34,373 |

|

| $22.19 |

| 204,526 |

| $57.8 million |

Total | 38,473 |

|

| $22.49 |

| 409,626 |

| |

| |

(1) | During the thirteen weeks ended December 30, 2018, we purchased 38,473 shares in order to satisfy employee tax withholding obligations upon the vesting of restricted stock. These shares were not acquired pursuant to any publicly announced purchase plan or program. |

| |

(2) | Weighted average price paid per share does not include any adjustments for commissions. |

| |

(3) | The weighted average price per share for shares repurchased under the share repurchase program during the period was $24.41, which does not include any adjustments for commissions. |

| |

(4) | On September 15, 2017, our Board of Directors authorized a $100 million share repurchase program of our outstanding common stock. The share repurchase program does not obligate us to acquire any particular amount of common stock and does not have an expiration date. As of December 30, 2018, $57.8 million remains available for repurchase under the current authorization. |

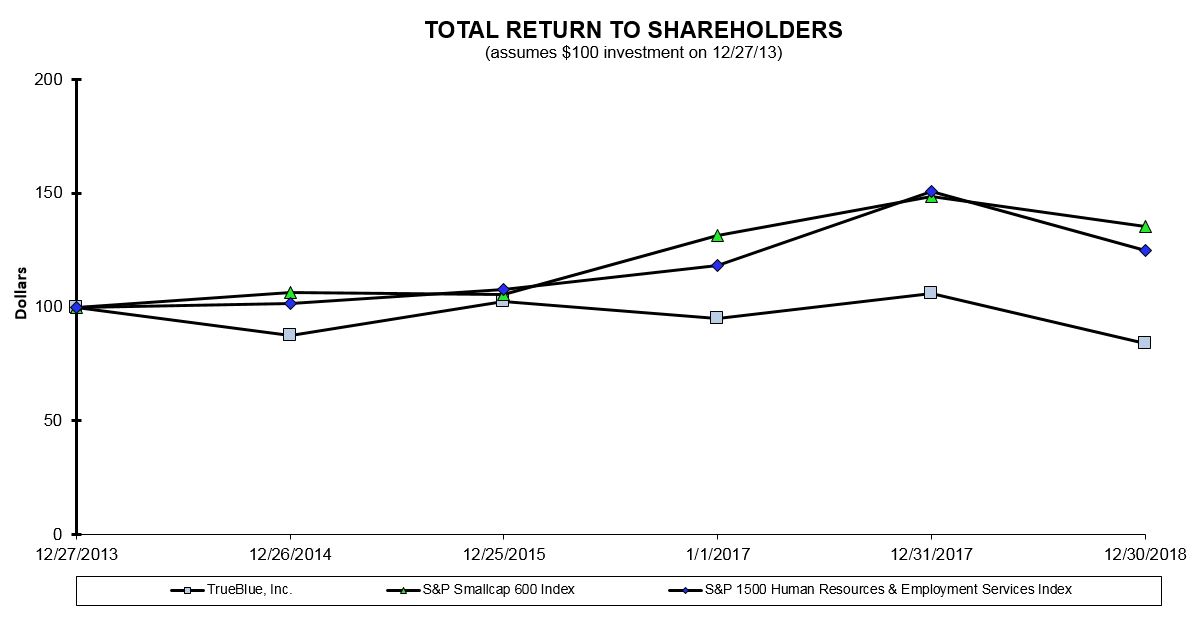

TrueBlue stock comparative performance graph

The following graph depicts our stock price performance from December 27, 2013 through December 30, 2018, relative to the performance of the S&P SmallCap 600 Index and S&P 1500 Human Resources and Employment Services Index.

All indices shown in the graph have been reset to a base of 100 as of December 27, 2013 and assume an investment of $100 on that date and the reinvestment of dividends, if any, paid since that date.

COMPARISON OF 5-YEAR CUMULATIVE TOTAL RETURN

|

| | | | | | | | | | | | | | | | | | |

Total return analysis | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

TrueBlue, Inc. | $ | 100 |

| $ | 87 |

| $ | 102 |

| $ | 95 |

| $ | 106 |

| $ | 84 |

|

S&P SmallCap 600 Index | 100 |

| 107 |

| 105 |

| 131 |

| 149 |

| 135 |

|

S&P 1500 Human Resources and Employment Services Index | 100 |

| 102 |

| 108 |

| 118 |

| 151 |

| 125 |

|

|

| |

Item 6. | SELECTED FINANCIAL DATA |

The following selected financial data is derived from our audited consolidated financial statements. The data below should be read in conjunction with Item 1A. Risk Factors, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Item 8. Financial Statements and Supplementary Data of this Annual Report on Form 10-K.

Summary consolidated financial and operating data

as of and for the fiscal years ended (1)

|

| | | | | | | | | | | | | | | | | |

Statements of operations data: | (52 weeks) | | (53 weeks) | | (52 weeks) |

(in thousands, except per share data) | 2018 | 2017 | | 2016 | | 2015 | 2014 |

Revenue from services | $ | 2,499,207 |

| $ | 2,508,771 |

| | $ | 2,750,640 |

| | $ | 2,695,680 |

| $ | 2,174,045 |

|

Cost of services | 1,833,607 |

| 1,874,298 |

| | 2,070,922 |

| | 2,060,007 |

| 1,637,066 |

|

Gross profit | 665,600 |

| 634,473 |

| | 679,718 |

| | 635,673 |

| 536,979 |

|

Selling, general and administrative expense | 550,632 |

| 510,794 |

| | 546,477 |

| | 495,988 |

| 425,777 |

|

Depreciation and amortization | 41,049 |

| 46,115 |

| | 46,692 |

| | 41,843 |

| 29,474 |

|

Goodwill and intangible asset impairment charge | — |

| — |

| | 103,544 |

| | — |

| — |

|

Interest and other income (expense), net | 1,744 |

| (14 | ) | | (3,345 | ) | | (1,395 | ) | 116 |

|

Income (loss) before tax expense (benefit) | 75,663 |

| 77,550 |

| | (20,340 | ) | | 96,447 |

| 81,844 |

|

Income tax expense (benefit) | 9,909 |

| 22,094 |

| | (5,089 | ) | | 25,200 |

| 16,169 |

|

Net income (loss) | $ | 65,754 |

| $ | 55,456 |

| | $ | (15,251 | ) | | $ | 71,247 |

| $ | 65,675 |

|

| | | | | | | |

Net income (loss) per diluted share | $ | 1.63 |

| $ | 1.34 |

| | $ | (0.37 | ) | | $ | 1.71 |

| $ | 1.59 |

|

| | | | | | | |

Weighted average diluted shares outstanding | 40,275 |

| 41,441 |

| | 41,648 |

| | 41,622 |

| 41,176 |

|

| | | | | | | |

Balance sheet data(2): | | | | | | | |

(in thousands) | 2018 | 2017 | | 2016 | | 2015 | 2014 |

Working capital | $ | 204,301 |

| $ | 215,860 |

| | $ | 176,668 |

| | $ | 314,989 |

| $ | 223,133 |

|

Total assets | 1,114,844 |

| 1,109,031 |

| | 1,130,445 |

| | 1,259,442 |

| 1,061,227 |

|

Long-term liabilities | 297,879 |

| 341,765 |

| | 354,131 |

| | 495,893 |

| 404,663 |

|

Total liabilities | 523,405 |

| 554,184 |

| | 605,266 |

| | 723,869 |

| 591,893 |

|

| |

(1) | In the fourth quarter of fiscal 2016, we changed our fiscal year-end from the last Friday in December to the Sunday closest to the last day in December. In addition, the 2016 fiscal year included 53 weeks, with the 53rd week falling in our fourth quarter. All other years presented include 52 weeks. |

| |

(2) | Fiscal years 2015 and 2014 data have been impacted by the adoption and retrospective application of ASU 2015-17, which classifies all deferred income taxes as non-current. |

The operating results reported above include the results of acquisitions subsequent to their respective purchase dates. In June 2018, we acquired TMP Holdings LTD. In January 2016, we acquired the recruitment process outsourcing business of Aon Hewitt. In December 2015, we acquired SIMOS Insourcing Solutions Corporation. In June 2014, we acquired Seaton. Additionally, in March 2018, we divested PlaneTechs, LLC.

|

| |

Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Management’s discussion and analysis of financial condition and results of operations (“MD&A”) is designed to provide the reader of our financial statements with a narrative from the perspective of management on our financial condition, results of operations, liquidity and certain other factors that may affect future results. MD&A is provided as a supplement to, and should be read in conjunction with, our consolidated financial statements and the accompanying notes to our financial statements.

OVERVIEW

TrueBlue, Inc. (the “company,” “TrueBlue,” “we,” “us” and “our”) is a leading provider of specialized workforce solutions that help clients achieve growth and improve productivity. We connected approximately 730,000 people with work during fiscal 2018, and served approximately 151,000 clients in a wide variety of industries through our PeopleReady segment which offers industrial staffing services, our PeopleManagement segment which offers contingent and productivity-based on-site industrial staffing services and our PeopleScout segment which offers recruitment process outsourcing (“RPO”) and managed service provider (“MSP”) services.

Fiscal 2018 highlights

Revenue from services

Total company revenue remained relatively flat at $2.5 billion for the year ended December 30, 2018, compared to the same period in the prior year. PeopleReady, our largest segment, returned to revenue growth. PeopleScout, our highest margin segment, delivered double-digit revenue growth. We acquired TMP Holdings LTD (“TMP”), increasing PeopleScout’s ability to compete for more multi-continent business. PeopleManagement, our lowest margin segment, declined primarily due to the loss of a significant customer and the divestiture of PlaneTechs, which further concentrated our focus on more profitable, higher-growth markets.

Gross profit

Total company gross profit as a percentage of revenue for the year ended December 30, 2018 was 26.6%, compared to 25.3% for the same period in the prior year. Our focus on lowering cost of services helped produce our third consecutive year of gross margin expansion.

Selling, general and administrative (“SG&A”) expense

Total company SG&A expense increased by $40 million to $551 million, or 22.0% as a percent of revenue for the year ended December 30, 2018, compared to $511 million, or 20.4% as a percent of revenue for the same period in the prior year. The increase in SG&A is primarily due to the added operating costs of the TMP acquisition, net of the PlaneTechs divestiture, together with transaction and associated costs of integration and divestiture. Increased SG&A expense also included continued investment in strategic cloud-based solutions and support for continued growth of the business.

Income from operations

Total company income from operations was $74 million, or 3.0% as a percent of revenue for the year ended December 30, 2018, compared to $78 million, or 3.1% for the same period in the prior year. The improved gross profit was largely offset by growth in SG&A expense.

Net income